These are certainly interesting times we live in. While the world is in the process of being completely transformed (in some ways for the better) due to the COVID-19 crisis, there has been an unequal response seen in the mobility ecosystem. In many ways the crisis has laid to bare the ongoing trends that have been brewing for some time.

Trends between Europe and the United States

These trends are related to the complete disruption that has occurred in the mobility sector over the past few years, such as 1.) disinvestment in public transport, 2.) over-reliance on VC funding for mobility startups, 3.) questionable business models, 4.) labor and employment status, and 5.) lack of public / private partnerships and coordination, and 6.) increase in individual auto usage and anti-urbanism. Each one of these have had massive implications for how new mobility ventures start, operate, and either succeed (or fail) in the long run.

However, another element to this acceleration of disruption, which is rapidly demonstrating the “winners and losers” is a clear distinction between markets and geographies. Specifically, what can be observed is a difference during and post COVID are new approaches to the mobility ecosystem between Europe and the United States.

Public transport usage

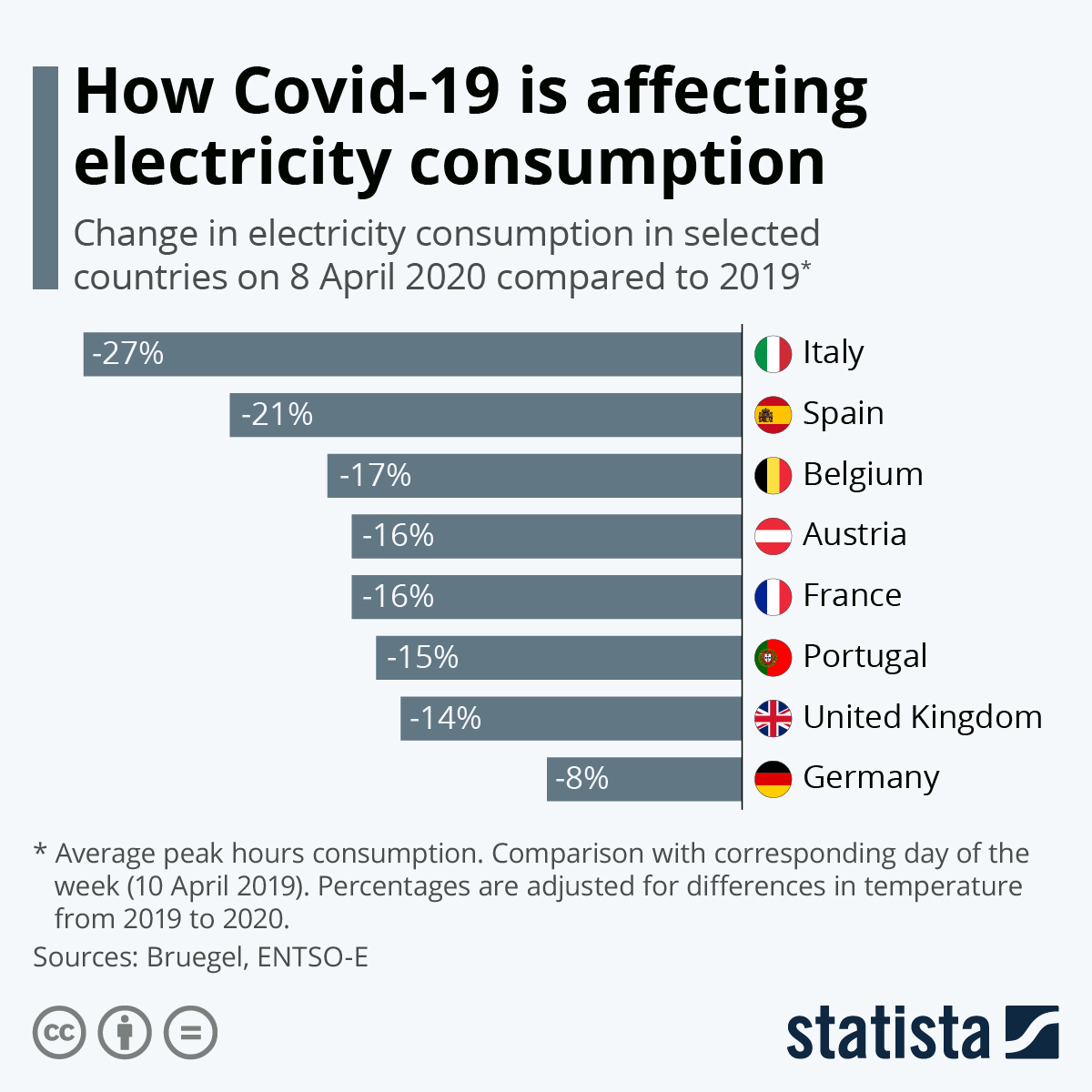

COVID-19 has proven to be an opportunity to rethink the very structure of our cities, and how we move around them. In Europe, while there is a massive decline in the usage of public transport, this is anticipated to be a temporary trend. Given the ubiquity of urban transport networks, this mode will experience a revival (albeit slowly and with social distancing measures in place) for commuters and visitors. In addition, the funding mechanisms for public transport from national authorities ensure more sustainable long term operations.

In the United States, we are seeing similar trends in a massive decline in public transport usage during COVID. However this process has been underway for the past decade or so. What the crisis has done is to solidify the marginalization of public transport as a primary mode of mobility in the United States. Coupled with a cultural aversion to cities (and government) it can be anticipated that further disinvestment will occur in this sector for at least the near term.

VC funding for startups

While European shared mobility startups have seen an increase in market capitalization over the past few years, and larger funding rounds, there has been a more incremental approach to the growth, expansion, and scaling of operations across the continent. Whether it be e-scooters, bikeshare, mopeds, or carshare, we have seen an approach that is more nuanced and aligned with market conditions.

On the other side of the Atlantic, mobility startups have been so heavily reliant on VCs as a lifeline for their “runways” that any hiccup in the market will cause major disruption. The same can be said for the COVID 19 crisis. We have seen a widespread failure on the part of multiple providers in the ecosystem, and most recently Lime received emergency funding from Uber (and assumed control of Jump bikes) in a deal that would prevent its complete collapse and bankruptcy.

Labor and employment

Labor and employment status on the part of full time workers and contractors has come under greater scrutiny given the ubiquity of shared mobility providers over the past few years. However, during the COVID 19 crisis, many of the startups have been able to weather the storm and keep a majority of their staff on the payroll, such as Bolt. While losing 75% in sales, Bolt has committed to not making a single layoff.

In the United States, we have seen the opposite trend in mobility-related employment. All of the major players have conducted massive waves of layoffs over the past 2 months, notably Uber, Lyft, Lime, etc. the most notorious of these was the Zoom call, which consisted of a scripted message to employees that they were to be terminated, followed up by instantly being locked out of their laptops.

Public / private coordination

Europe has witnessed positive trends towards public private coordination in the mobility ecosystem leading up to the COVID-19 crisis. Voi was a leader in proactively reaching out to Nordic governments to obtain permission to operate, and Tier has taken a similar approach in developing unique partnership models and promoting the usage of public transport within its user experience.

However, many of the US-based mobility providers have taken an approach (to both the North American and European markets) that is “ask for forgiveness, not permission”. This is an unsustainable strategy and business model and when we return to a reopening of the economy, operators that run roughshod over the public sector will more than likely continue to fail.

Individual auto usage and anti-urbanism

While is is true there are currently many more automobiles on European streets and highways in the past few weeks as governments have started opening up, this is not a trend that is completely single modal. To counterbalance this, there has been a massive increase in walking and cycling, both of which are being promoted by urban design schemes being implemented in Milan, Brussels, London, Barcelona, Berlin, etc. On top of this, we do not see an “emptying of the city” as a result of the crisis.

What is now observed in the United States overall is a rapid acceleration of single car usage, promotion of individual mobility, and a rejection of cities (and density) as a whole. As was seen the in the rapid depopulation of New York City to other regions of the United States during the COVID-19 crisis, it can be extrapolated that fear of shared mobility and urbanized settings (which has been a part of the cultural fabric for centuries) is only being reinforced and will continue post-crisis.

There are of course many deviations and anomalies that can be seen as counter to the high level trends and comparisons described previously. However, what can be said is that there are clear differences based on geography, culture, and segmentation between Europe and the United States that expose how our cities and mobility as a whole will fit into the landscape as we experience a “return to normalcy.”

The Urban Mobility Daily is the content site of the Urban Mobility Company, a Paris-based company which is moving the business of mobility forward through physical and virtual events and services. Join their community of 10K+ global mobility professionals by signing up for the Urban Mobility Weekly newsletter. Read the original article here and follow them on Linkedin and Twitter.

Corona coverage

Read our daily coverage on how the tech industry is responding to the coronavirus and subscribe to our weekly newsletter Coronavirus in Context.

For tips and tricks on working remotely, check out our Growth Quarters articles here or follow us on Twitter.